A growth strategy is vital for successful market growth. The way to achieve substantial market penetration and profitability is through a sustainable growth strategy framework.

The Jobs-to-be-Done growth strategy framework provides invaluable ways to help your business structure its ideas as it grows.

How to Define Your Brand’s Growth Strategy with Jobs-to-Be-Done

You need to evolve your product line and grow your business. But how will you go about getting there?

- Want to add a new feature set to your existing products?

- Can I develop a new low-cost product?

- Can we create a new platform-level solution that gets the job done significantly better? Is it significantly cheaper?

- Something else entirely?

It can seem like a guessing game.

Thankfully, there’s a more predictable, less risky framework to help you decide on your path to boosting your market share. Disruptive innovation and other innovation strategies can be applied more predictably through the lens of Jobs-to-be-Done.

When we use the Jobs-to-be-Done framework to examine product successes and failures, we observe the same phenomenon time and time again:

New products and services win in the marketplace if they help customers get a job done better (faster, more predictably, with higher output) and/or more cheaply.

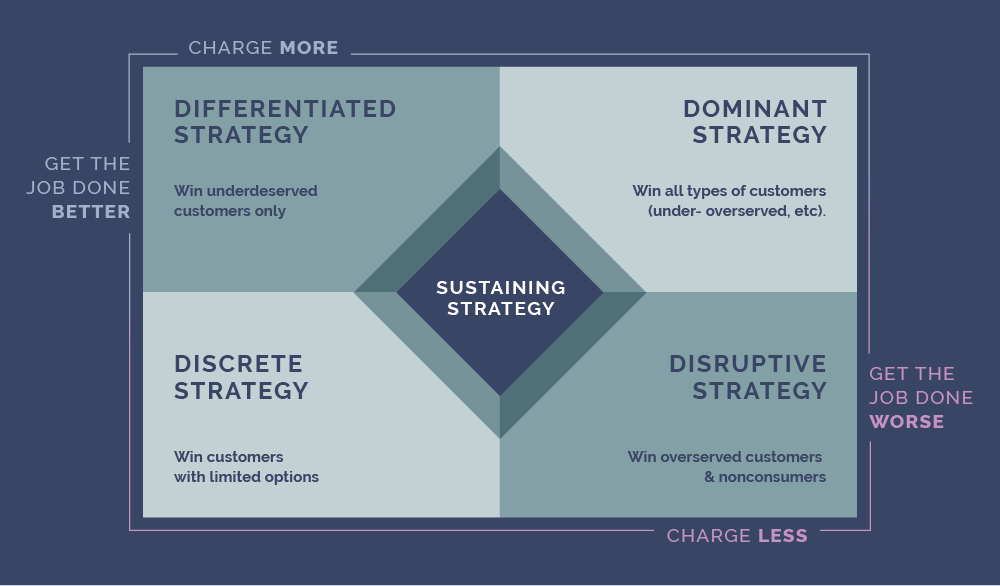

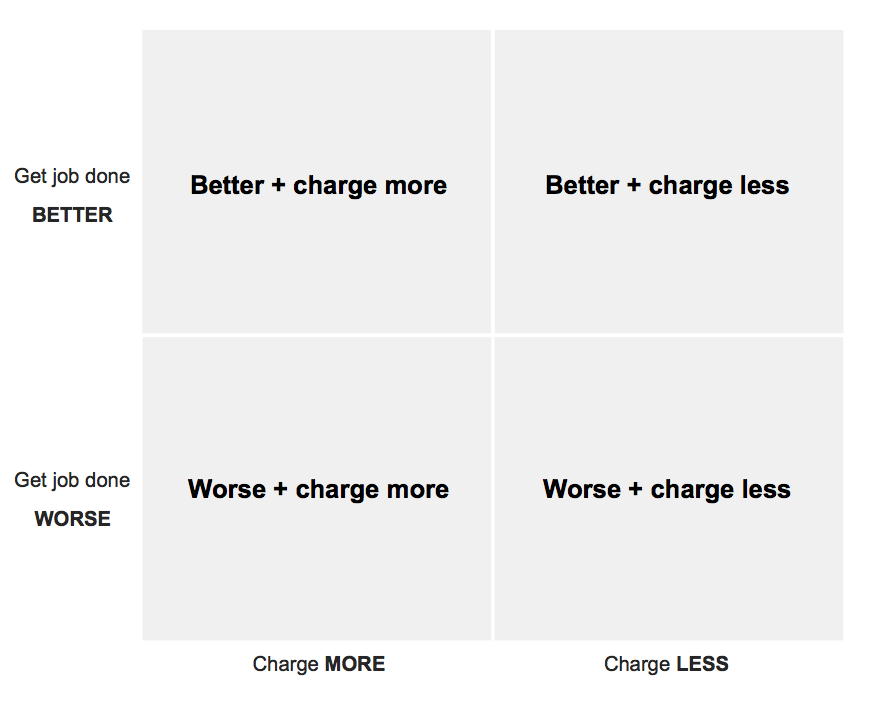

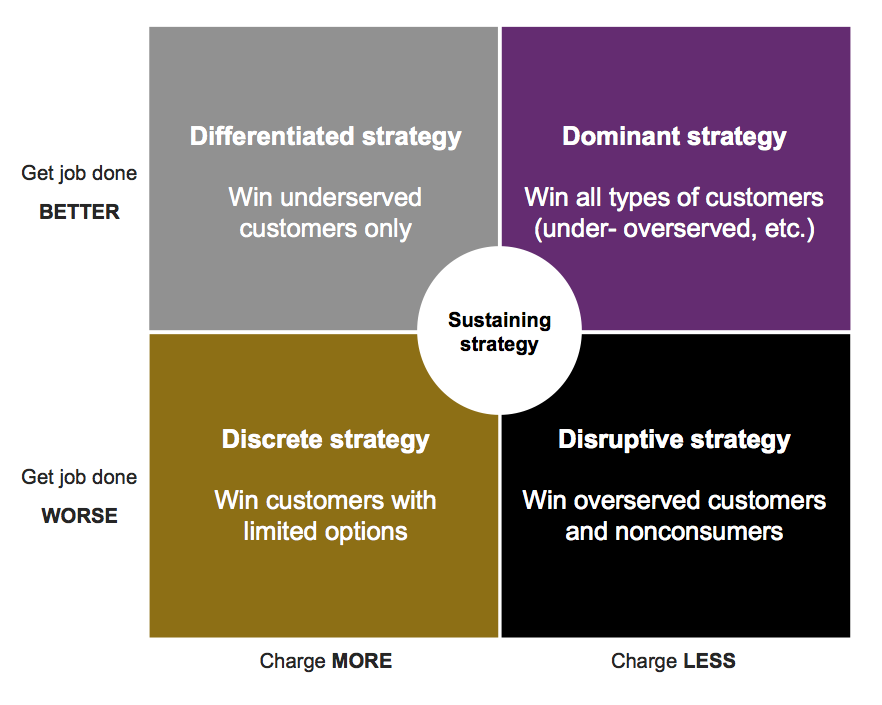

This matrix suggests that every product or service your company creates will fall into one of five categories and serve certain customer segments.

1. Better and more expensive. This type of innovation will only appeal to underserved customers. These are customers who have unmet needs and are willing to pay more to get a job done better.

2. Better and less expensive. A better-performing, less expensive product will appeal to all customers.

3. Worse and less expensive. A worse-performing, less expensive product will appeal to over-served customers (those with no unmet needs). It will also appeal to non-consumers—people whose current solutions don’t involve the market at all, or who are not even attempting to get the job done as they cannot afford any of the existing solutions.

4. Worse and more expensive. A worse-performing, more expensive product will only appeal to customers for whom limited (or no) alternatives are available. This happens in unique or atypical situations.

5. Stuck in the middle. These products only get a job done slightly better or slightly cheaper. This kind of product probably won’t attract any new customers. It’s a poor strategy for a new market entrant, but it may help an incumbent company retain existing customers.

Seems pretty straightforward so far, right? But how do you use this information to generate predictable growth?

The 5 Growth Strategies

Each of these five situations warrants its own distinct growth strategy—so we defined five approaches any company can adopt in the quest to win in a market.

1. Differentiated growth strategy

You’ll want to pursue a differentiated strategy when you discover a population of underserved consumers that you want to target with a new product or service offering that gets their job (or multiple jobs) done significantly better, but at a significantly higher price.

Examples include Nest’s thermostat, Nespresso’s coffee and espresso machines, Apple’s iPhone 2G, the Herman Miller Aeron chair, Whole Foods’ organic food products, Emirates airlines’ international flights, Bang & Olufsen’s personal audio products, BMW sports cars, Sony’s PlayStation (original model), and the Dyson vacuum cleaner and Airblade hand dryer.

2. Dominant growth strategy

Take this approach when you want to target all consumers in a market with a new product or service offering that gets a job done significantly better and for significantly less money.

Examples of offerings that successfully employed a dominant growth strategy include Google Search, Google AdWords, UberX, Netflix’s streaming video, Progressive Insurance’s non-standard automobile insurance, and Vanguard Group’s personal investment services.

3. Disruptive growth strategy

You’re pursuing a disruptive strategy when you discover and target a population of over-served customers or non-consumers with a new product or service offering that helps them to get a job done more cheaply—but not as well as competing solutions.

Think Google Docs (relative to Microsoft Office), TurboTax (relative to traditional tax services), Dollar Shave Club’s razor offering (relative to Gillette), eTrade’s online trading platform (relative to traditional financial brokerages) and Coursera’s online educational services (relative to traditional universities).

4. Discrete growth strategy

You are pursuing a discrete strategy when your brand targets a population of “restricted” customers with a product that gets the job done worse, yet costs more. This strategy can work in situations where customers are legally, physically, emotionally, or otherwise restricted in how they can get a job done.

Examples of offerings that successfully employ a discrete strategy include drinks sold in airports past security checkpoints, stadium concessions at sporting events, check-cashing and payday-lending services, and ATMs in remote locations.

5. Sustaining growth strategy

When your company introduces a new product or service offering that gets the job done only slightly better and/or slightly cheaper, you’re pursuing a sustaining strategy. Examples of offerings that successfully employ a sustaining strategy are plentiful.

The Jobs-to-be-Done Growth Strategy Matrix

We can sum it all up in a simple graphic. Strategyn created the Jobs-to-be-Done Growth Strategy Matrix to give you an easy-to-reference illustration of when and how you should use these strategies to grow in your desired markets.

Jobs-to-be-Done Theory and ODI are integral to successful product planning — they enable a product planner (or a marketer, engineer or developer) to conceptualize a product or service that will win in the marketplace BEFORE it is approved for development. Applied correctly, it results in predictable innovation, as the conceptualized offering is certain to address unmet customer needs.

The key to picking the winning strategy is being able to discover under- and over-served segments of customers and determining if they are willing to pay more to get the job done better.

With this framework, you can understand your past successes and failures through a new lens—and can adopt a strategy to create winning products and services in the future.

Grow Your Business With Jobs-to-be-Done

Developing strategies for growth is essential. It gives your business the latitude to focus on new markets. Use any of the jobs-to-be-done growth strategies against your business model, and you can rest assured that you will be headed in the right direction. It will not only give you peace of mind, but it is also a practical way to increase the chances of successfully expanding your business.

Want to learn more about how this JTBD Growth Strategy Matrix works and how to apply it for growth in your business? Check out this explainer video: